Meteoric advance of Asian giants threatens the production of affordable electric vehicles in the West and already causes layoffs in American factories

China has consolidated its hegemony in the global market for batteries for electric vehicles, controlling about 70% of world production by 2025. The accelerated advance — a significant jump from less than 50% recorded in 2021 — poses an unprecedented logistical and commercial challenge for Western automakers, which now structurally depend on Asian technology to make their fleets viable.

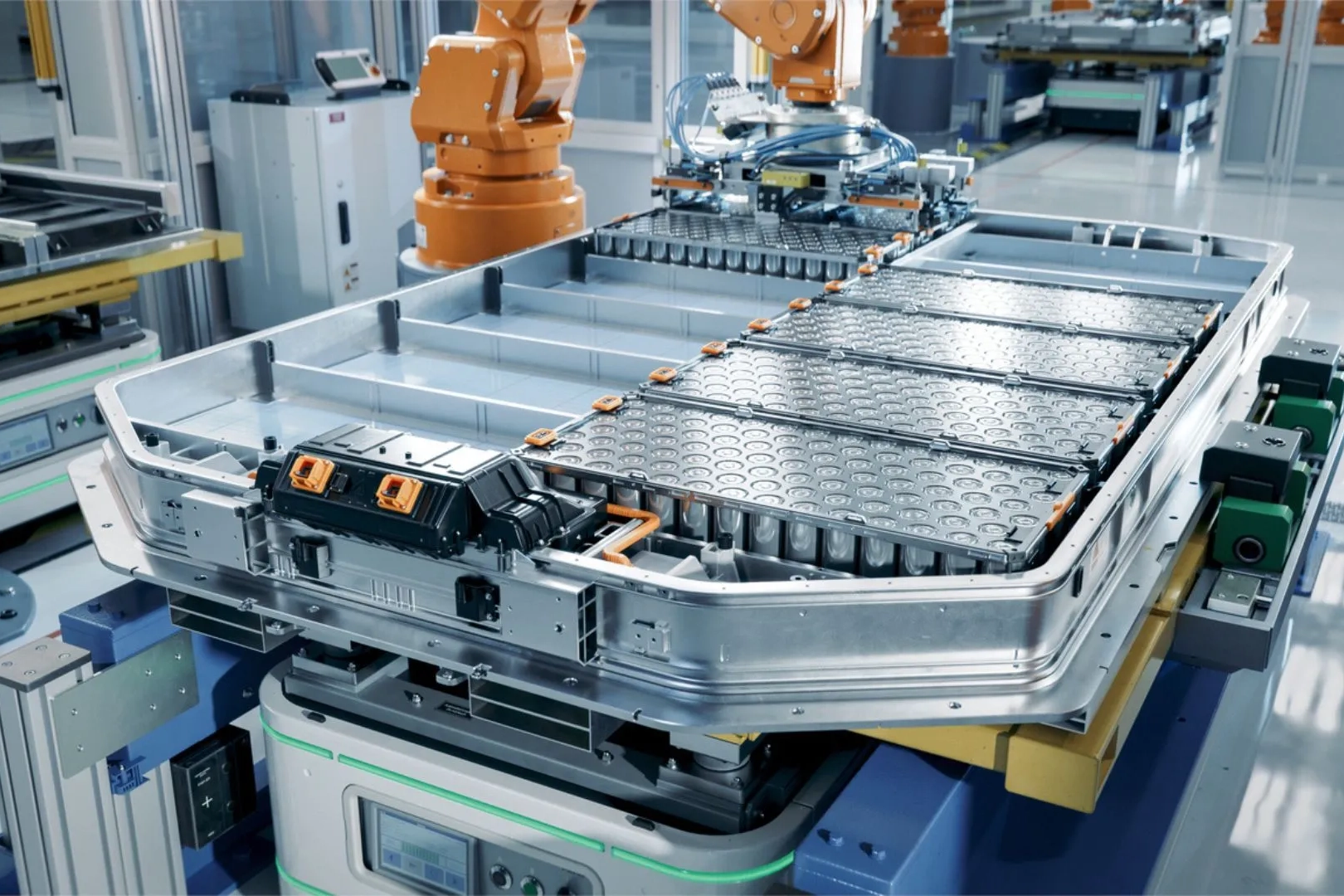

Chinese dominance is evidenced by the ranking of the main global manufacturers. Of the ten largest companies in the world in terms of installed capacity, six belong to the Asian country. CATL has maintained its sole industry leadership, supplying components for heavyweight Western models. The giant reported a record net profit of 72.2 billion yuan (about $10.4 billion) in 2025, up 42% year-on-year.

Right behind CATL is BYD. In addition to equipping its own vehicles, the brand has expanded the supply of cells to competitors such as Stellantis and Xiaomi, strengthening its presence with new fronts in Hungary and Turkey.

SEE ALSO:

In contrast to the shielding of Chinese companies, which have low exposure to the United States market, South Korean manufacturers are experiencing a severe retraction. Companies such as LG Energy Solution and SK On have felt the brunt of slowing EV sales in North America, resulting in asset restructurings at Ohio plants and layoffs at plants in Georgia.

China’s strategic advantage raises a red flag: by monopolizing the production chain, Beijing gains the power to dictate the global minimum price of batteries. Experts point out that this concentration makes it difficult for American automakers to launch affordable electric cars, in the competitive range of US$ 30,000.

Despite the 28% drop in global electric sales between January and February 2026, dependence on China remains the main bottleneck in the West. Without rapid production expansion at home or in allied countries, manufacturing costs outside Asia will remain high, restricting electrification to higher-income niches.